Investors of all walks of life should not only pay attention to specific company, industry or real estate developments, but also to other macroeconomic developments that could determine the performance of all financial assets in the future. Changes in interest rates have had a material impact on stock prices and the current bull market in U.S. equities is evidence of its impact as it has benefited from historically low interest rates. Corporations have used much of their cheap money to buy back their respective stock and full a big part of the bull market. However, when an inversion of the yield curve happens, it usually signals an ominous short-term future. In August, this phenomenon occurred and investors were quick to conclude that an economic recession was imminent. Since trade tensions have eased, phase one of the trade deal between the U.S. and China is close to being signed and the FED cut the FED funds rate, the yield inversion has disappeared. Are we out of the woods?

What does an inverted yield curve mean?

The yield curve is the connection between the yields of all maturity lengths of soverign debt issued by a central government; in this case we are referring to U.S. treasuries with a maturity from one month (short-term) to 30 years (long-term) that can be bought and sold on the secondary market. The spread between short- and long-term rates provides a strong indication of how investors feel about the level of risk. U.S. treasuries are viewed as the least risky investments, except for cash, therefore their returns or yield are lower than equity (stocks or business interests) and higher risk debt (corporate debt, mortgages or loans). U.S. treasuries are considered a safe haven when investors are fearful of a recession. The U.S. government has never defaulted on its debt and has the ability to run deficits or raise taxes, therefore theoretically it can never miss a payment.

An inverted yield curve occurs when there is higher demand for long-term debt than normal that leads to long-term yields falling below short-term yields. Investors favor longer dated U.S. treasuries during bad times because interest rate movements cause greater changes in the value of the long-term debt than short-term debt, therefore investors are hoping not only to avoid losses in equities, but also gain from the appreciated value in long-term U.S. treasuries. This leads lenders to lend less because lenders do not want to borrow short and lend long when the interest rate differential is low or negative, which is called a credit crunch.

If investors collectively chose to shift investments from equities and high risk debt to U.S. treasuries, then the values of equities and high risk debt will fall. If this goes on for too long, individuals and corporations will hold off on spending (personal consumption and business investment is 87% of U.S. GDP) and soon enough a recession will be realized.

However, an inverted yield curve alone cannot predict an imminent recession, although it has successfully predicted most recessions in U.S. history. The yield curve is no longer inverted and that is because the FED cut the FED fund rate. If the FED did not cut, the U.S. yield curve would still be inverted. It is important to note that this phenomenon happens before a recession is realized.

Is the U.S. economy in bad shape?

The U.S. government has estimated that the U.S. gross domestic product (GDP) grew at an annual rate of 1.9% in the third quarter of 2019, following 2.1% annualized growth in the previous quarter. This is a slowdown from the 3.1% growth recorded in the first three months of the year. The main growth drivers were personal consumption and government spending. Business investment declined by 3%, which was the sharpest decline since early 2016.

The trade tensions between the U.S. and China caused a significant amount of uncertainty and businesses deferred investment until there was more clarity on the trade deal outcome. I believe businesses are still waiting because even though there is a tentative trade deal, there is no clear understanding of its impact. Many businesses are moving forward as usual but are doing so cautiously while considering investments outside the U.S. and China in case trade optimism is a facade.

FED Chair Jerome Powell said on October 30th, “Trade policy tensions have waxed and waned, and elevated uncertainty is weighing on U.S. investments and exports,” he said.

The director of research at the Economic Policy Institute, Josh Bivens, said in July, “There is plenty to worry about as there is a weakness in both residential and non-residential investments. The last time residential construction investments contracted for this long was during the great recession.”

The U.S. economy may be close to a tipping point and there are signs of a slowdown. The question is, was the trade war the main cause of the slowdown or is it masking fundamental economic problems? Think about it. Why would any two countries argue and dispute economic inequality if there were no underlying economic problems. Equity markets generally price in such developments and future expectations in advance, but for now the S&P 500, Dow and NASDAQ are all reaching new highs. So are investors ignoring some of the earlier warning signs?

The FED might be caught in a liquidity trap

Many analysts polled by Reuters believe that central banks of many countries are in a liquidity trap. This occurs when an injection of cash into the financial system fails to stimulate the economy because the cash is not invested into business expansion, which leads to long-term growth in GDP. Many investors expect deflation or slow economic growth and would rather wait for better opportunities. This belief by investors is a self-fulfilling prophecy that leads to the bad economic outcome they were preparing for and thus investors expect more stimulus from their central bank to get them off the sidelines and invest in expanding businesses.

In the case of the U.S., if the FED fails to lower the FED funds rate enough to spur business investment, then you can see how this will play out. Low interest rates forever.

Will lower interest rates do any good?

The Fed lowered rates by 25 basis points (0.25%) in October, the third cut of 2019. Even though this dovish stance might raise questions of whether or not were headed towards a recession, the U.S. is in a relatively strong position compared to other countries. Japan has not met its inflation targets even with negative rates. Germany is on the verge of entering a recession despite negative rates. China was slowing down before the trade tensions. The European Central Bank (ECB), which is in Germany, further reduced its rates to -0.5% and 40% of investment-grade debt outside the U.S. have a negative yield.

The short-term rates in the repo market recently shot up and the FED has been trying to keep a lid on it by providing a significant amount of liquidity. The repo market crisis that took place is evidence that the risk of a recession is heightened. The FED had to inject more than $75 billion into the system in September to provide the necessary liquidity into the market and appears they are not done providing liquidity.

Typically low rates have contributed to positive growth in the economy. However, a recent research report (“Low-Interest Rates, Market Power, and Productivity Growth” by Liu, Mian and Sufi) shows that low interest rates will lead to slower economic growth through increased market concentration.

This report states that even though lower rates usually encourage firms to invest more, it only benefits the market leaders rather than small players. Consequently, the largest investors crowd out smaller investors as the long-term rates fall. According to the research, when the rates decline, large investors are able to quickly grab opportunities and gain more market share, thus disincentivizing smaller investors in taking risk. This then means the economic benefit from lower interest rates flows mostly to a select group that has so much wealth, there is no pressure to spend or invest that would increase GDP until the most optimal opportunities are manifested.

Real estate is a great example. When mortgage interest rates fell to new lows a few months ago, did you take advantage of that opportunity? Did you lock in those low rates of that borrowed money and invest it into something that had a better return than the interest on the loan? If you said no to both of those, then you didn’t do what the FED was expecting. Is it because you don’t have enough equity in your home? Is it because you don’t have a down payment? Were you denied because of bad credit or a high debt-to-income ratio? Is the home you wanted now too expensive because low rates caused rapid inflation? As you can see, small players have less ability to take advantage of lower rates.

In the short-term, the decision by the FED to cut rates will provide some boost, but such benefits will not last long.

Stagnating wage growth and debt at all-time highs

Wage growth for the private sector was 2.9% in September 2019 compared to September 2018.

Jared Bernstein, an economist, stated that although wages for blue-collar workers and non-managers grew by 3.5% in September 2019, this number is stagnating. Slower wage growth with little change in inflation will negatively affect consumers’ ability to spend.

Sarah House, an economist at Wells Fargo, believes a meaningful strengthening of wage growth cannot be expected in the short-term.

The total debt in the U.S. was $22.6 trillion in September. It has increased by more than 750% from 1989 to 2019.

Kimberly Amadeo, the president of World Money Watch, said the Social Security Fund will not have enough to cover the retirement benefits as promised and, as a result, Congress is more likely to curtail benefits than raise taxes in the future. Government spending is about 17% of GDP. If anyone thinks raising taxes will solve our problems then look no further to the stock market rally after federal income taxes were dropped from 35% to 21%. If you did the opposite, what do you think would happen?

This rising debt burden could also lead to financing problems for the government in the future.

I could go on here and mention that corporate debt is more than double what it was at the peak before the financial crisis. We could discuss the student loan crisis. Lets’s not forget the home affordability crisis in every major metropolitan area of the U.S. Or let’s ignore the report that a $500 surprise expense would put most Americans into debt. Americans have binged on more than Netflix, they binged on cheap debt. Let’s suffice it to say most Americans are tapped out and this credit fueled economic expansion could end horribly for those not prepared.

Is the U.S. heading toward a recession?

Since the invention of the FED in the U.S., there has been a strong correlation between inverted yield curves and recessions, although with a time lag of 12 to 18 months. The U.S. yield curve inverted every time before a recession since 1950.

The spread between three-month and 10-year U.S. treasuries began falling in 2014 and inverted for three months in mid-2019 (June to August). This inversion was the first time it had occurred since 2007, shortly before the realities of the financial crisis set in. The curve rebounded back into positive territory in October and has since continued to widen.

The past three recessions occurred within a year after the yield curve rebounded from an inversion.

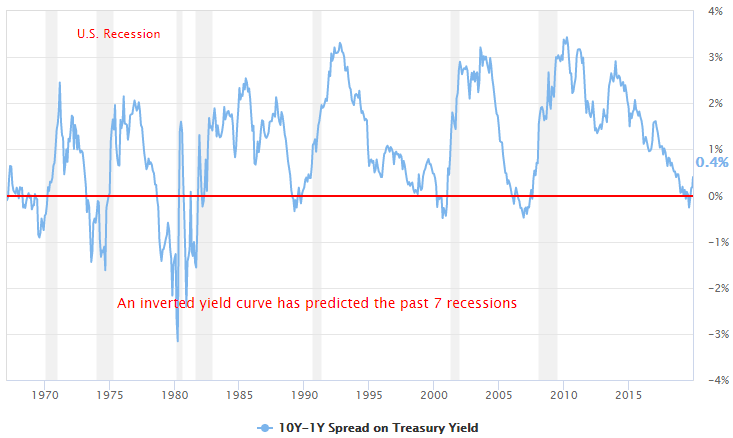

Below you will see a graph plotting the spread between the 10-year and 1-year U.S. treasury. The gray bars represent recessions and the red line represents zero.

Each time the yield curve inverted (negative; below the red line), the U.S. went into a recession in about 10 to 18 months later. It is general accepted that a downturn would occur at most 24 months from the first inversion.

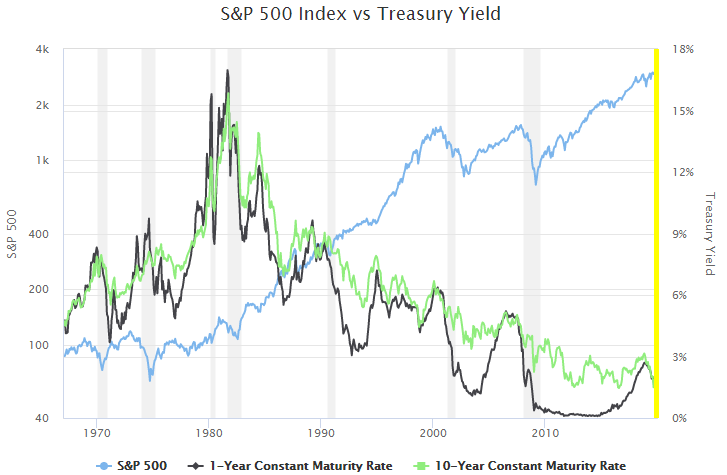

The S&P 500 index has historically rallied during a yield curve inversion, posting positive returns. Phillip Nelson, the head of asset allocation at NEPC in Boston, says that inversions are a part of the late-cycle of an economic expansion and they do not represent the end of a cycle. Therefore, equity markets can continue to provide positive returns. The one exception was in early 2000 when the bear market and inversion occurred very close to the same time.

The S&P 500 index has hit a record high every time an inversion occurred, therefore inversions do not first occur at 52 week lows for example.

The following graph shows the 10-year and 1-year U.S. treasury spread and the S&P 500 Index together.

Are we heading for a recession? You be the judge.